NeXusAvicultura

Market Analysis | May 2026

Whole chicken at €7.50, half at €4: the meteoric success of chains such as Master Poulet, Pouletos and PB-Poulet Braisé is rekindling an uncomfortable question for the entire European poultry sector: when price is king, what happens to traceability and consumer trust?

The smell of roast chicken has become, in just a few years, a constant feature of many working-class neighbourhoods in Paris, Lyon and Marseille. The so-called halal rotisseries — outlets specialising in whole roast chicken, with halal certification and aggressive pricing — have gone from being a curiosity to a large-scale commercial phenomenon. Master Poulet claims more than 36 points of sale, Pouletos operates 35 and PB-Poulet Braisé accounts for 31. Looking at the volumes of chicken sold (cooked) by these rotisseries, and focusing solely on the Master Poulet franchise — founded in 2019 by entrepreneur Chouaib Benbakir — the chain reports having sold more than 10,000 tonnes of chicken in 2025 with estimated turnover above €30 million, and a franchise entry cost of just €10,000–€15,000 that is fuelling near-breakneck expansion.

But behind the lit display cases and the almost identical menus — half chicken at €4, whole chicken at €7.50, thigh at €2.50, drumstick at €1 — several reports in the French press — Le Point, RMC-BFM, Capital, as well as numerous online outlets — have focused on a grey area that directly affects European poultry: the true origin of the meat and compliance with the French labelling regulations in force since 2025.

A whole roast chicken at €7.50 cannot come from a premium French farm. The arithmetic of production costs is unforgiving: when price is king, the origin is usually outside the country that consumes it.

Clear regulations… and compliance that falls short

Since 1 March 2022, and reinforced by successive measures, France has required food service establishments — including takeaway outlets — to indicate to consumers the country of origin of the poultry, pork and lamb they serve. The transposition and tightening of the decree in February 2025 extended and consolidated this obligation.

The rule, on paper, admits no ambiguity: customers must be able to see, without asking, where the animal was born, raised and slaughtered.

The reality on the ground is very different.

A survey by the French interprofessional body ANVOL found that only 15% of restaurants were complying with the obligation to display the origin of poultry meat. In recent field inspections carried out at six roast chicken rotisseries in Paris, not one was respecting the rule. A single independent establishment in the 19th arrondissement displayed a halal certificate — from a Polish supplier, Storteboom Hamrol Sp. — which had the peculiarity of having expired more than a year earlier.

When staff were asked about the origin, answers ranged from “France, sometimes Belgium”, “mainly Poland and Spain”, “an excellent European chicken” or, simply, silence. Master Poulet’s own director, Nabil Bahar, acknowledged to the press that the meat comes predominantly from Poland and Spain, arguing that no French supplier would be capable of meeting the daily volumes the chain requires at the price it offers.

15% of French restaurants comply with the obligation to label chicken origin.

The remaining 85% operate in a grey area that consumers do not always detect until a controversy erupts.

The macro figures confirm the context

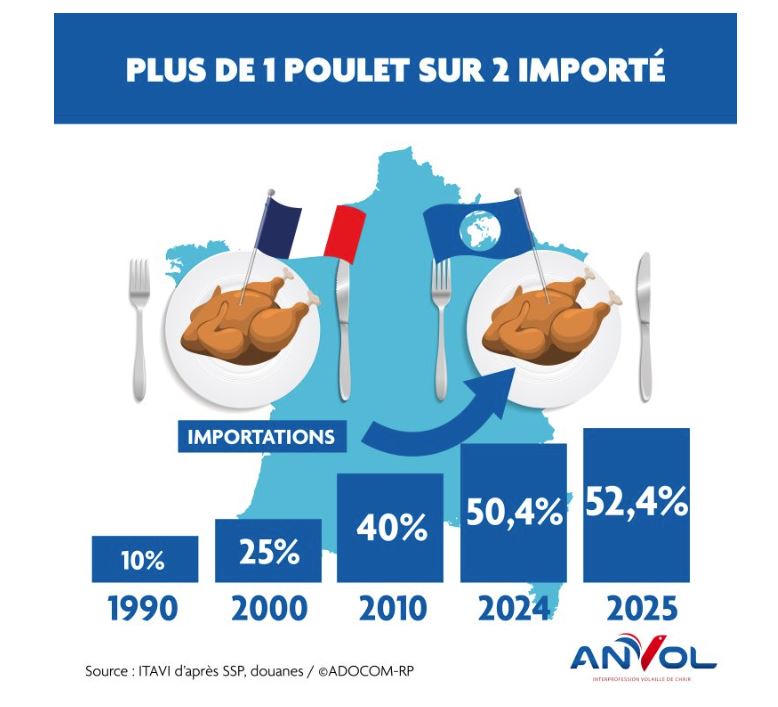

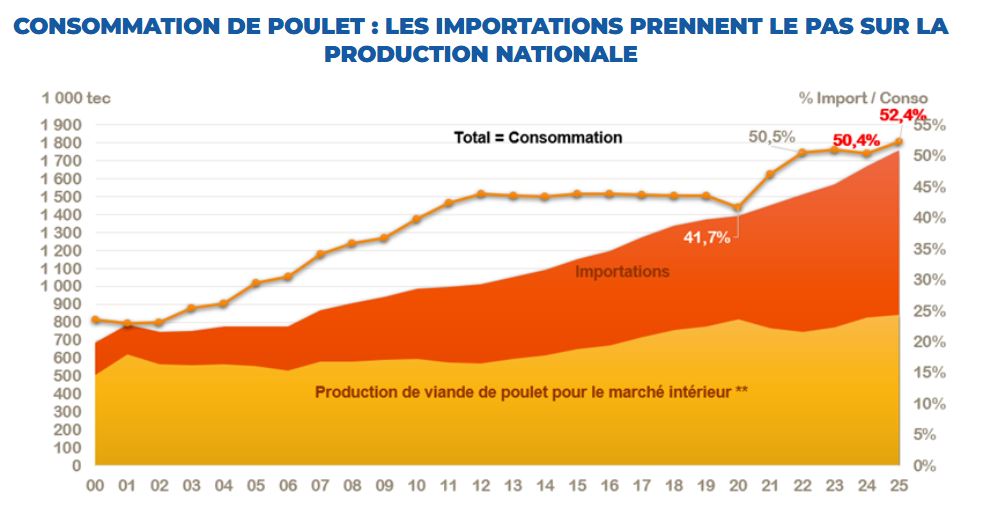

Far from being an isolated case, the phenomenon fits like a clockwork piece into the statistical picture that the French administration itself publishes each year. According to official Agreste data (French Ministry of Agriculture), in 2024, 43.0% of all poultry meat (chicken + turkey + duck + guinea fowl…) consumed in France was imported, a figure that rises to 50.1% when looking at chicken alone. Twenty years ago that proportion stood at around 20%.

in 2024

1 in every 2 chickens consumed

in france was imported

Broken down by origin, data from the ANVOL interprofessional body and French customs confirm that Poland is the leading supplier with more than 253,500 tonnes carcass weight equivalent per year (and rising), followed by Belgium (207,000 t) and the Netherlands (132,700 t). It is also the case that part of the chicken invoiced as “Belgian” or “Dutch” actually originates from Ukraine, Brazil or Thailand, but enters the EU through the ports of Rotterdam or Antwerp and is re-labelled after initial processing.

The product most affected by imports is the breast fillet (close to 370,000 tonnes per year), followed by thighs (142,300 t) and prepared products (140,500 t). These cuts — used intensively by the food service sector and the processing industry — are precisely those that underpin the low-cost model. Fresh whole chicken barely accounts for 3% of imports: the so-called “poulet du dimanche” remains, for the most part, French.

Table 1. Structure of the French chicken market in 2024

| Indicator | Value / Share |

| Poultry meat consumed in France that is imported | 43.0% |

| Chicken consumed in France that is imported | 50.1% (1 in every 2) |

| Leading supplier: Poland | >253,500 tcwe / year (≈40% of imports) |

| Second supplier: Belgium | 207,000 tcwe / year |

| Third supplier: Netherlands | 132,700 tcwe / year |

| Restaurants complying with the origin labelling obligation | ≈15% |

| Annual growth of the halal market in France | 5–10% |

Source: compiled from Agreste (GraphAgri 2025), ANVOL, FranceAgriMer and Wikipedia (Master Poulet).

Why Poland and Spain, and not France

The explanation is structural and deserves to be examined honestly. Poland has for several years been the European Union’s leading chicken producer, accounting for more than 22% of Community output, and maintains a cost advantage that makes it the most competitive European supplier. The average price differential with France is €0.70 per kilogram — a sufficient margin for a low-cost food service model to systematically favour Polish supply or, to a lesser extent, Spanish supply.

Spain, the EU’s third-largest producer after Poland and France, has poultry operators with certified halal lines that have successfully positioned themselves in a growing segment. The Basmahal brand from Grupo Uvesa — which controls integrators such as UVESA-MHP and, more recently, Payán Hermanos — offers cured halal chicken charcuterie and fresh product with recognised certification. The penetration of Spanish and Italian product into chains such as Master Poulet, according to corporate sources and sector databases, is supported by both price and logistics (refrigerated transport reaching Paris in under 24–36 hours).

France, by contrast, has been losing relative competitiveness for twenty years. Its broiler production has grown by 9% over two decades, while consumption has doubled. The French Senate itself, in its report on the competitiveness of “la ferme France”, concluded that one in every two chickens consumed daily by French people is no longer of French origin. The domestic industry is specialising in the premium segment — Label Rouge, IGP, organic — while the bulk of food service (RHD) and processing demand is met by imports.

Poland produces 22% of EU chicken at a cost €0.70/kg lower than France. Spain adds certified halal capacity and logistical proximity. France, meanwhile, is abandoning the volume segment to retreat into the premium tier.

Halal and traceability: two debates that are not the same

It is worth bringing clarity to the discourse, as media noise tends to conflate two independent issues. Halal certification is a religious seal governing the method of slaughter and chain separation on the production floor; when issued by recognised bodies (in Poland, MHA or IFANCA; in Italy, Halal Italia; in Spain, the Instituto Halal of Junta Islámica) and kept current, it provides clear religious guarantees. The problem observed in field inspections is not halal per se, but certificates that are expired, absent or not displayed.

Traceability is an entirely different matter: it is the ability to know where an animal was born, raised, slaughtered and processed, as well as the welfare conditions and production method applied. A product can be perfectly halal while simultaneously originating from an intensive system with high stocking densities. Conversely, a French Label Rouge chicken meets the highest animal welfare standards without being, save for exceptions, halal. Conflating both dimensions in the public debate distorts the conversation and, worse still, leads consumers to suspect a religious certification when what is actually failing is the system for providing information on origin.

The true weak point of the low-cost model is not the halal ritual but the opacity of the supply chain: multiple suppliers, occasionally expired certificates, EU labelling mechanisms that allow extra-Community product to be reclassified as “EU origin” after simple reprocessing, and rapid rotation of origins driven by daily spot market prices. This is where the French regulator — and, by extension, the European regulator — has unfinished business.

Implications for the European poultry sector

The halal chicken case in France is symptomatic of broader tensions affecting the entire Community poultry sector. First, it confirms that the low-cost food service segment will continue to grow — the French halal market is expanding at 5–10% per year — and that its economic logic inevitably drives the search for lower-cost origins. Second, it highlights a latent reputational cost: when a traceability controversy erupts, the damage falls not only on the chain in question but on all imported product, and by contagion on the entire poultry filière of the exporting country.

Poland, Spain and the Netherlands export to France with all the health and quality guarantees required by Community regulations. However, the public image of Polish or Spanish chicken in the French consumer’s mind — reinforced by reports associating imports with élevage intensif and opacity — risks eroding the perception of a product that, in health terms, passes the same controls as French chicken. The poultry interprofessional bodies of exporting countries should take note.

For the European producer, the lesson is twofold. On the one hand, there is a volume market — halal and food service — that demands competitively priced product and where Spanish and Polish integrators hold a solid position that should be defended through active transparency. On the other hand, there is growing demand for information: 88% of French people say they trust the traceability of French chicken, and 90% associate the national bird with food sovereignty, according to recent surveys. That preference will sooner or later translate into additional regulatory pressure, already foreshadowed in the French decree of February 2025.

88% of French consumers trust the traceability of domestic chicken. 50% of the chicken they consume is not French. This gap between perception and reality is the true structural problem of French poultry farming — and the primary opportunity for European exporters that commit to transparency.

European poultry does not compete globally on price: it competes on standards. And standards only generate value when they are visible. The day a rotisserie in Paris can show customers, alongside the halal certificate, a smart label reading “European chicken from country X, Welfair-certified farm, fed without deforestation soy, slaughtered on 28 April at plant XX”, the traceability conversation will have changed direction entirely. And it will not be a concession: it will be a competitive advantage.

SUMMARY

| Case | Boom of low-cost halal rotisseries in France (Master Poulet, Pouletos, PB-Poulet Braisé) |

| Master Poulet founder | Chouaib Benbakir (2019); chain with ≈36 points of sale and 30+ M€ in turnover |

| Typical prices | Whole chicken: €7.50 | Half chicken: €4 | Thigh: €2.50 | Drumstick: €1 |

| Declared actual origin | Poland, Spain, Italy, Netherlands (to varying degrees depending on chain) |

| Critical issue | Traceability: widespread non-compliance with mandatory origin labelling |

| Regulatory framework | French decree (1 March 2022, extended February 2025): mandatory origin labelling in food service |

| Actual compliance | ≈15% of restaurants (ANVOL survey) |

| French chicken import rate | 50.1% of chicken meat consumed (Agreste, 2024) |

| Halal market growth | 5–10% per year in France |

| Sectoral challenge | Turning traceability into a competitive asset rather than a reputational liability |

The opportunity: making traceability a competitive asset

It is tempting for the Polish or Spanish sector to view the French furore as someone else’s problem, an internal regulatory matter for a neighbouring country. That would be a mistake. The narrative taking hold in France — low-cost chicken = imported chicken = opaque chicken — ultimately damages broiler producers who scrupulously comply with European welfare, health and halal certification standards.

The major Spanish integrators with halal lines, whether for domestic consumption or international markets, have a unique opportunity to take the lead: current and digitally verifiable halal certification, transparent labelling with QR codes enabling the end consumer to trace the farm of origin, proactive communication with food service clients on animal welfare standards, and active participation in European regulatory debates on traceability. The same applies to Polish producers such as Cedrob, Drosed, SuperDrob and the Cedrob-Konspol group, whose reputational challenge in France is greater but so too is their capacity to respond.

European poultry does not compete globally on price: it competes on standards. And standards only generate value when they are visible. The day a rotisserie in Paris can show customers, alongside the halal certificate, a smart label reading “European chicken from country X, Welfair-certified farm, fed without deforestation soy, slaughtered on 28 April at plant XX”, the traceability conversation will have changed direction entirely. And it will not be a concession: it will be a competitive advantage.

To find out more:

-. Poultry farming in France

-. Poultry farming in Europe

- A historic victory for French broiler farmers (origin decree, February 2025)

- French consumers reaffirm their preference for poultry meat and prioritise French origin

- Growth in 2024 and 2025 of European broiler production

- 2026 overview of the European chicken market

- 2025 map of broiler production: key trends